For most working adults, retirement is an abstract concept. A typical retirement age is somewhere around 65, meaning the average worker has decades to accumulate their assets before entering the next chapter of their life. However, planning for retirement can still feel daunting and difficult – like a constant uphill battle. How do you know if you will have enough money? Will you need to change your lifestyle to make your money last? Here, we boiled down the retirement puzzle to its barest bones, adding some clarity to a complicated task.

Retirement planning is incredibly complicated. There are too many factors to consider: saving, spending, inflation, investment returns, life expectancy. Many of these are unknowable. It’s no wonder many people ignore retirement planning all together. Still, it’s important to think through this at a basic level.

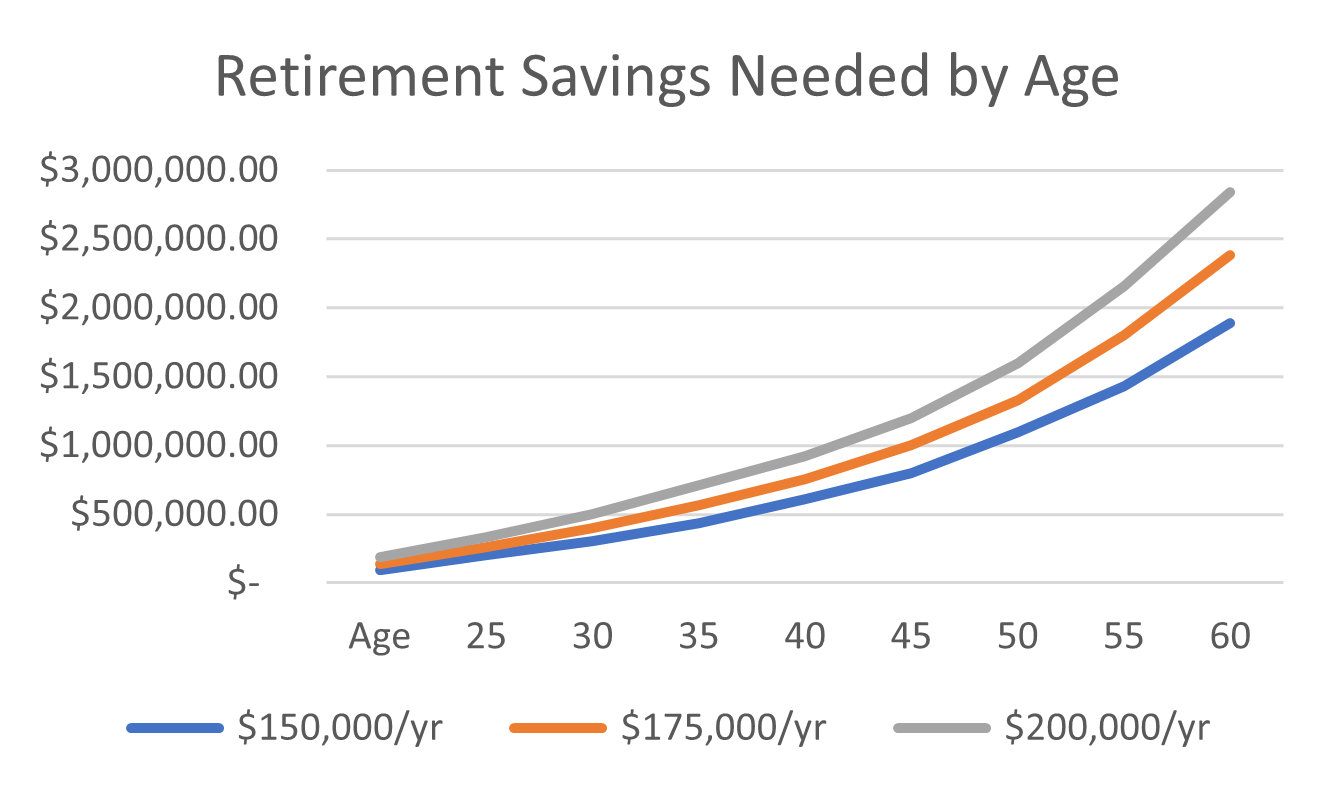

The following chart illustrates the relationship between age, income, and your pot of savings needed to continue that income into retirement. We make assumptions on savings rates, inflation, and investment returns – all of which impact the outcome. We believe most people would be happy to continue their current level of spending into retirement. Only the most frugal of us choose to forgo a large amount of spending to live lavishly in the future.

Pick your age and pick your income, this table shows how much you need in savings to be “on track.” Once you “hit” your number, this assumes you still need to continue to save and invest until retirement. While we think our assumptions are reasonable as a rough guide, these shouldn’t be taken as gospel.

Wealth can only be defined relative to what you spend. What may seem like a sizeable retirement nest egg may not suffice if one wants to spend at a high clip in retirement. A 65-year-old desiring $250,000 in retirement income, needs over $3.8 million saved, but only needs $2.8 million if $200,000 in retirement income is desired.

This table also highlights that saving early in life benefits from time and compounding returns. Consider a household earning $150,000. At age 25, the investor will need to have around $92,000 saved to be on track to retirement. The same household would need over three times as much saved just 10 years later.

It becomes harder to catch up later in life. Take two investors with the same income of $150,000; one is 35 and the other is 45. They start saving for retirement at the same time. The 45-year-old investor would need to save over 30% more each year than the younger investor. For most, saving 30% more of their current income would be hard to swallow.

What causes this exponential difference over time? The answer lies in compounding returns.

More than a Snowball’s Chance

Think of compounding returns like rolling a snowball down a mountain. The younger investor starts at the top of the mountain where their snowball has the most potential to grow before reaching the bottom. An older investor starts halfway down the mountain effectively missing out on all of the snow above them. The same is true for retirement savings. With more time, each dollar has more potential to grow and compound until needed for retirement. Time is the single most powerful and accessible tool afforded to all investors.

Although we cannot alter the passage of time, there are other levers investors can pull to change the trajectory of their retirement. For example, you can make a small lifestyle change now and increase your savings rate. An investor may be able to improve their lifestyle in retirement or leave an inheritance to their beneficiaries if they even save an additional 1% early in the accumulation phase. For a young 25-year-old investor saving 1% more, the same would only need $87,000 to be on track to retire, or $5,000 less than the original example.

What It All Means

Take advantage of time as much as possible and reap the benefits when it comes time to retire. Money saved early takes advantage of a lifetime of compounding. It’s a lot easier to compound money than increase savings later in life.

Contact us at 865-584-1850 or info@proffittgoodson.com

1 This chart and corresponding graphics have been developed for illustration purposes only and should not be relied upon to make investment decisions. There are a variety of assumptions used in this exercise that are subject to change, especially over a long time horizon. Portfolio returns vary and are not meant to represent Proffitt & Goodson, Inc.’s performance. Consult a financial professional for a personalized assessment.